When a man’s suit fits, when the construction is beautiful, when the sewing and fabrics are there… in the end, you’ll look the best in it.

John Varvatos, American Designer

In a previous article (see Performance Based Contracting vs Outcomes Based Contract vs Relational Contract) I said that from my perspective there is no difference between Performance Based Contracts and Outcomes Based Contracts. Moreover, in the same article I said for “Generation 3 PBCs”, that these also included relational contracting features.

Since this article there has is continuing emphasis by some organisations and advisors towards “Outcome Based Contracts”, including saying these were different to PBCs. As such, I wanted to revisit this in light of the continued discussion on the similarities and differences.

Firstly, we need to understand what we mean by outcome. Typically, supporters of Outcomes Based Contracts say it is about simply having buyers define the desired outcome and letting sellers tender their innovative solutions independent of the buyer telling them how. Using this definition, an outcomes based contract can have PBC elements (i.e. a well-considered and defined risk-reward structure that drives the seller to deliver the buyer’s outcome) in addition to relational elements (i.e. a relational / behavioural charter, no fault dispute resolution clauses, etc.). Alternatively, an outcomes based contract could simply be a conventional contract based on well-known and standard commercial principles using deliverables and milestones for payment.

In some of the commercial arrangement I have dealt with we have very deliberately separated the buyer’s outcome from the contract outcome. In this case, the buyer’s intended outcome, say putting a ship to sea, may include aspects outside of the direct control or even influence of the seller including the buyer’s own processes and staff, and third-party sellers. We call this level the ‘enterprise’ to distinguish it from the contract level. In this case so while both buyer and seller are clear about the enterprise outcome, which may include collaborative behaviours, it is not feasible to ask sellers to offer a contract solution, innovative or otherwise, for how to do this that doesn’t involve a significant exclusions / business rules or financial risk premiums making any solution unaffordable.

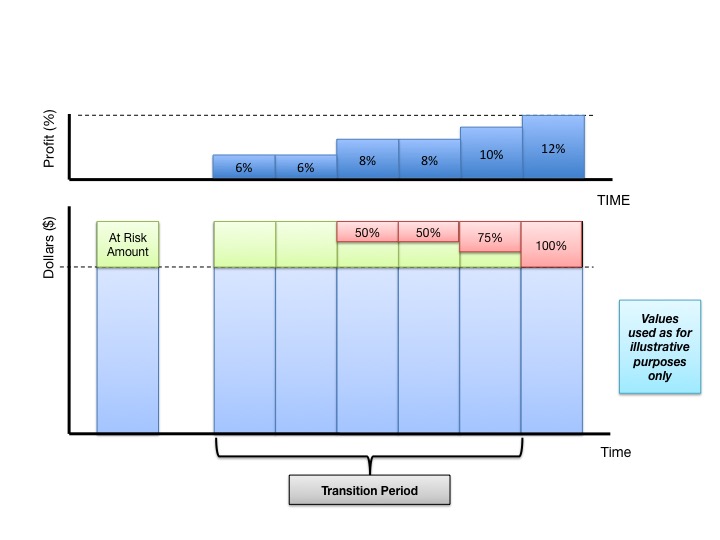

That said, we have developed many PBCs that, using different tiers of performance measures that link to different risk-reward structures (consequences). You can find out more about how to do this from the following article (see When is a KPI not a KPI?).

So as with many things in life, it is not simply one or the other. Outcomes based contracting focuses on describing the buyers need and how to solve it; in this case by not constraining the solution. However, an outcomes based contract can include both performance and relational elements. Alternatively, PBCs can focus on the delivery of outcomes, including enterprise outcomes, which include collaborative behaviours.

So in the future, when you are considering what type of commercial arrangement you want to use, whether outcomes based, performance based or relational, I urge you to think about what features you need as opposed to the label put on it. Since like a well-tailored suit, it is skill of the tailor and quality of the material as opposed to the label that makes it a perfect fit.