In the previous article (see Starting a PBC – Part 1) I looked at the need and benefits of using a transition period when starting a Performance Based Contract (PBC). In this article I will look at key considerations to using a transition period when starting a PBC including examining the effect of the transition period on the PBCs Risk-Reward balance.

During a transition period the performance measures can either be implemented (i.e. turned on):

- all at once; or

- phased in over differing times either individually or as groups (e.g. start all supply support performance measures once all the spares part have been bought and delivered).

Additionally, more complex PBCs can also include:

- specific ‘transitional’ performance measures that only apply during the transition period, or

- setting performance levels at a lower performance level during the transition period recognising the need to balance the buyer’s need to hold the seller accountable for some level of performance (even if lower than the final performance level) and the seller’s need to minimise commercial risk during the implementation.

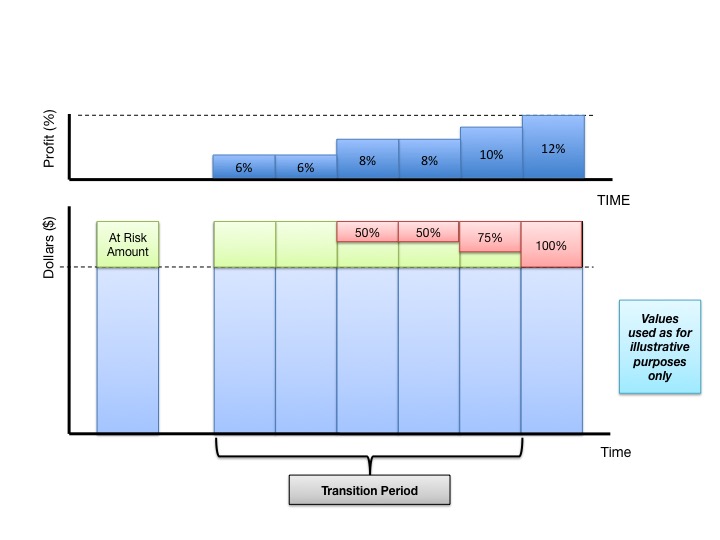

As part of designing the transition period it is also important to balance risk and reward. If the seller is ‘protected’ against non-performance (i.e. paid 100% of the At-Risk Amount regardless of performance) the commercial risk is different and the buyer may want to vary the commercial rewards during the same period. One option many PBCs now use is to ‘shape’ the profit margin during the transition period to reflect the change in commercial risk. This approach is illustrated in Figure 1. Please note that the values used in Figure 1 are for illustrative purposely only and are not recommendations or represent the values in real PBCs.

Figure 1 – PBC Transition Period and Shaped Profit

Important factors to consider when using a shaped profit margin approach:

- While profit shaping commences with the start of the contract the seller can choose an early exit from the transition period. For example, instead of having a 6 month transition period the seller could choose to only have a 3 month, or indeed no, transition period and access the full profit margin from day 1.

- The variation in profit (fee) must be enough to motivate seller’s acceptance of the additional risk (if any). That is, if the difference is too small or the original base profit margin is too high, there may be insufficient reward for the seller to take on the additional commercial risk and exit the transition period.

- Ensure that variation in shaped profit is linked to other Risk-Reward structures within the contract (e.g. contract extension, stop payment, termination, etc.).

- Consider whether the profit (fee) varies with individual performance measures, groups of performance measures or all performance measures.

In summary, the use of a transition period when starting a PBC is a critical step in establishing the right recording, scoring, reporting and reviewing cycles. However, applying a transition period is not a simple as having 12 months without consequences. Instead, it requires both buyer and seller to understand what outcomes they are seeking in the use of a transition period and to tailor it to specifically meet this need.