Business, that’s easily defined – it’s other people’s money.

Peter Drucker

In addition to using the Basis of Payment as a method for shaping the cost behaviour of the seller it is also possible to use a “cost” performance measure as part of a Performance Based Contract (PBC). By using a “cost” performance measure it is possible to force the routine discussion of cost performance between buyer and seller as part of the overall performance management strategy.

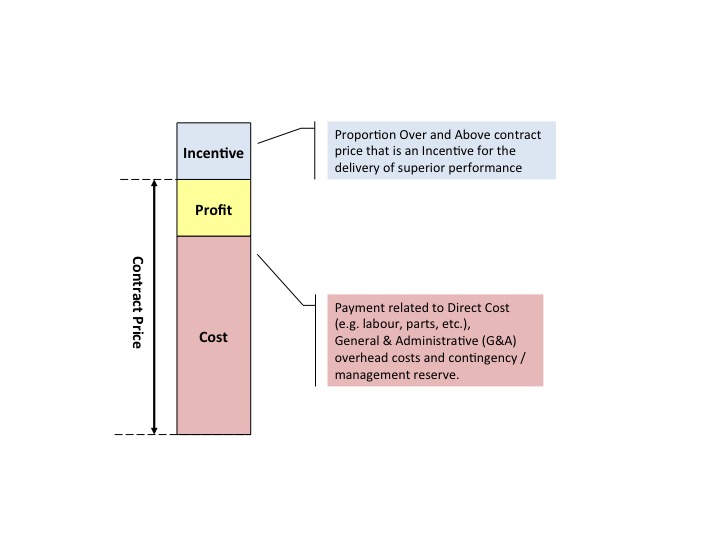

In this discussion it is important to understand that while we may refer to “cost” this typically reflects the overall cost to the buyer (e.g. the total amount of money paid to the seller, usually called “price”) as opposed to the seller’s cost that does not typically include General and Administrative (G&A) overhead costs (e.g. those indirect overhead costs such as human resources, security and IT functions, etc.), profit associated with this activity or contingency / management reserve (e.g. an amount of money set aside by the seller to cover those unexpected costs). Figure 1 illustrates the difference between contract price and cost, and the various elements that make up contract price.

Figure 1 : Cost vs. Price

Typically these “cost” performance measures represent either the cost of the services / products delivered under the contract (e.g. $1,000,000 for the delivery of 1,000 flying hours per year for an aircraft) or that same services / products delivery cost per unit (e.g. $1,000 per flying hour).

Alternatively, rather than measuring the cost of the services / products delivered, the cost can reflect the “enterprise” Total Cost of Ownership (TCO) which can be defined as the total cost to deliver the capability regardless of organisation undertaking the activity. This includes costs associated with both operations and support including engineering, maintenance and logistics, training, etc. Importantly, if a TCO performance measure is going to be used, it is essential that it captures all costs regardless of organisation including any resources applied by the buyer (e.g. the cost associated with the buyer’s operations team). Similar to the “cost” performance measure, the “enterprise” TCO cost performance measure it can take two forms; TCO or TCO per unit.

Regardless of which type of cost performance measure used there are three key points that need to be considered as follows when designing a “cost” performance measure. Specifically, the performance measure must:

- not distract the seller from meeting its performance obligations under the contract (e.g. while cost may be important, so is the delivery of the contract performance);

- produce real and effective improvements to the support of the capability without detriment due to aggressive cost saving (e.g. at worst case, contain future contract cost without changing the contract performance levels); and

- provides sufficient incentive to the Contractor to achieve the cost outcome (e.g. link to a reward or remedy in the PBC such as increasing (or decreasing) contract duration).

Where “cost” performance measures form part of the performance measure hierarchy they are typically not related to any form of financial consequences, either positive or negative (e.g. a Key Performance Indicator (KPI) using our terminology). Instead, they form part of the Strategic Performance Measures (SPM) reflecting an “enterprise” focus on overall TCO for the capability.

In our experience, where a cost performance measure, especially an “enterprise” TCO performance measure, has been included as part of the overall performance management strategy we have observed better cost outcomes as the “enterprise” is forced to routinely discuss the topic of cost. The question really should be, can you afford not to include a cost performance measure?